Investigative Reporting on India’s External Debt (2014–2024)

Staff Writer: Susmita Ghosh

Published on: March 5, 2026, 5:20 p.m.

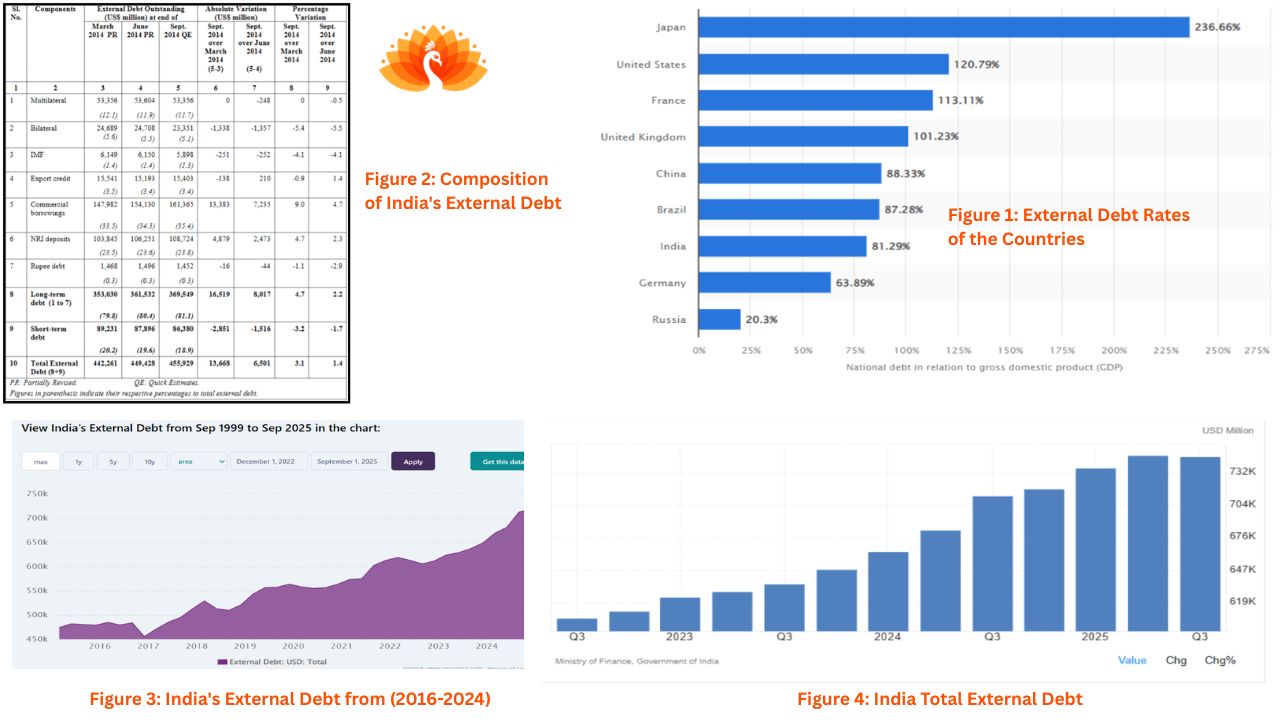

External debts are now becoming a primary concern for various countries. When a country’s debt portion is lent from foreign lenders such as commercial banks, governments or international financial institutions are known as External Debts. But, there is a shocking side to this external debt. If any country cannot or refuses to pay back money it borrowed from foreign sources such as from banks or other countries then this will be said to be in sovereign default. This means the government has failed to meet its debt obligations. This will lead to stop providing further essential resources or assets or any kind of loans or financial aid in future because they no longer trust the country to repay. Figure 1 showing India’s external debt although increasing overall but also decreasing as a percentage of Gross Domestic Product or GDP. This is a positive signal for economic health. However, as the Indian economy is growing faster than its borrowing, the Debt-to-GDP ratio fell from 23.9% to 18.7%. Figure 1 indicates that India’s Debt-to-GDP ratio (81%) is moderate but higher than Germany and still significantly safer than the US or Japan. Therefore, external debt is a highly serious concern and it acts as a critical barometer for the nation's macroeconomic stability and its ability to withstand global financial shocks. When Indian entities such as the government, corporations and banks borrow money from foreign sources then it is referred to as India’s external debt. This debt is divided into three main components: public sector debt government and public enterprises), private corporate debt and multilateral and bilateral loans. Apart from these, there are other types of debts which include short-term and long-term debts. Figure 2 showing total external debt at the end of September 2014 stood at US 455.9 billion of India. This marks an increase of US 13.7 billion or 3.1%, compared to March 2014. Figure 2 observed long-term external debt exhibited a positive trend and this growth was primarily driven by increases in commercial borrowings and Non-Resident India (NRI) deposits. However, the multilateral trend remained stable and witnessed no change from March 2014. Apart from these, the export credit showed a minor negative adjustment. Therefore, Figure 2 showed a strategic shift for India's external debt at end-September 2014 towards a more stable long-term debt profile. The evidence observed from Census and Economic Information Center (CEIC) regarding India External Debt represents the most prominent pattern and supports the sharp rise in the borrowing from 2023 to 2024. With the help of External Commercial Borrowings (ECBs) this growth was primarily driven. Figure 3 further showed that, “valuation effect” played a role since the US dollar fluctuated against the rupee and the total debt figure frequently appeared higher or lower in dollar terms regardless of new borrowings. India’s debt-to-GDP ratio remained stable and sustainable in nature irrespective of raising absolute numbers. Figure 4 further illustrates that India’s Total External Debt from 2023 was steady and followed an upward trend. Due to this upward trend, various Indian states faced significant fiscal challenges due to high levels of external and internal debt leading to intense political confrontations between State and Central Government. The Kerala Government filed a suit in the Supreme Court against the Union Government under Article 131 in December 2023. In this case, Kerala argued the Union violated federal principles by restricting its borrowing capacity to INR 26, 226 crores less than required. This causes a severe liquidity crisis. On April 1, 2024, the Supreme Court refused to grant interim relief to Kerala to borrow more money immediately. The Court referred the case to a five-judge Constitution Bench to decide on significant questions regarding the scope of federal fiscal relations and whether the Union can restrict state borrowing. Punjab's fiscal situation, as highlighted by its October 2023 debt moratorium request, presents a complex picture of both deep-seated challenges and potential avenues for fiscal recalibration. However, the state grapples with a significant “legacy debt” burden impacting negatively. Chief Minister Bhagwant Mann indicates a substantial portion of new borrowings over ₹27,016 crore was solely allocated for the service interest on inherited loans. This perpetuates a cycle where borrowing is used to repay existing debt rather than for productive capital investment, leading to a projected total outstanding debt exceeding ₹4 lakh crore by 2026. Populist spending, such as free electricity schemes costing ₹20,000–₹22,000 crore annually, further strains the budget, with nearly 75% of revenue receipts consumed by "committed expenditures" like salaries, interest, and pensions in FY 2023-24. This has resulted in a high debt-to-GSDP ratio of approximately 46.8% in 2023-24, one of the highest in India, and a liquidity crunch that led to a 38% shortfall in capital outlay for developmental projects, as noted by the Punjab CAG report (2024). The state's revenue mismatch, where a 15.4% growth in own tax revenue was offset by a 33% decrease in central grants and the cessation of GST compensation, exacerbates these financial pressures. The Prime Minister has been requested by the Chief Minister to provide a five year moratorium on the payment of debts. He also insisted that the Centre release ₹5,637 crore of Rural Development Funds (RDF) it holds to point out the dire fiscal situation that the state is in and its desperate need of greater fiscal flexibility to drive growth. Therefore, between 2014 and 2024, the standard macroeconomic indicators of India remained unchanged, while its debt-to-GDP ratio decreased, although its absolute foreign debt increased. Although the growth of the nations was at a faster pace than borrowing, some states like Kerala and Punjab were in a liquidity crisis which was fueled by old debts and excessive expenditure. This has led to the emergence of legal and political arguments between state and central governments, which highlight a desperate tension between state financial responsibility and financial independence at the state level.